Monthly Market Summary

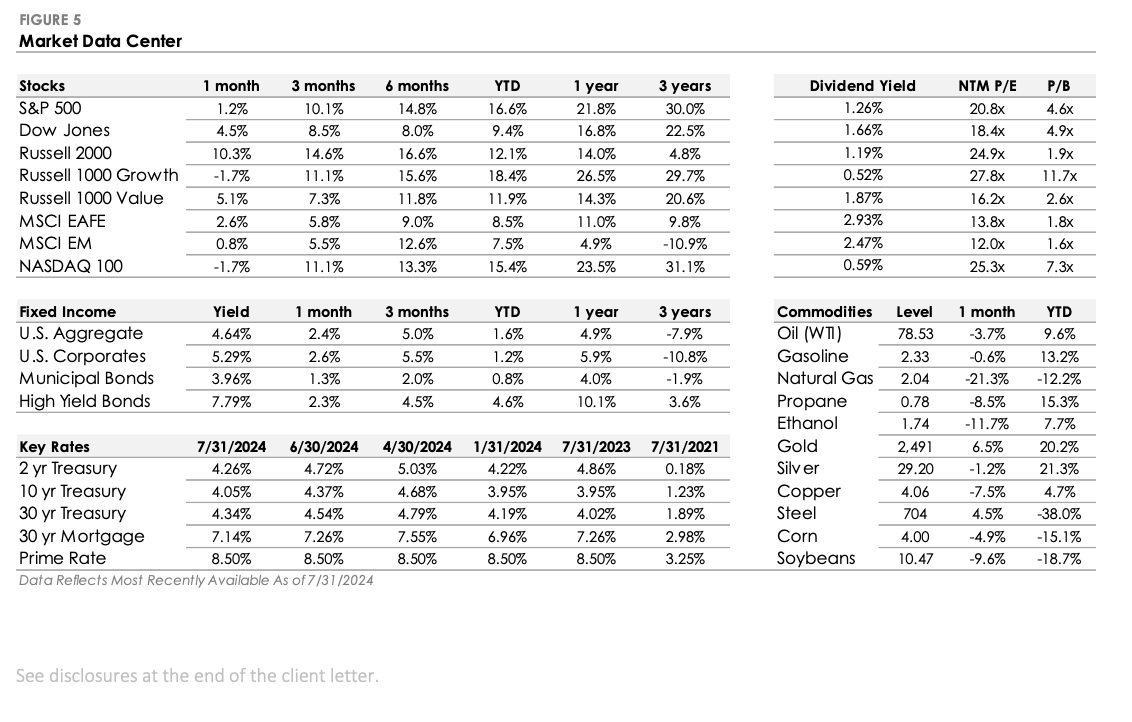

The S&P 500 Index returned +1.2% in July, underperforming the Russell 2000 Index’s +10.3% return. Ten of the eleven S&P 500 sectors traded higher, led by Real Estate, Utilities, and Financials. Technology was the only sector to trade lower, reversing a portion of its rise in the first half of 2024.

Corporate investment-grade bonds produced a +2.6% total return as Treasury yields declined. Corporate high-yield bonds gained +2.3% as credit spreads tightened.

International stock performance was mixed. The MSCI EAFE developed market stock index returned +2.6%, while the MSCI Emerging Market Index returned +0.8%.

Stocks & Bonds End the Month Slightly Higher

The S&P 500 ended July slightly higher, its third consecutive monthly gain. The index initially traded higher and briefly surpassed 5,600 for the first time before it traded lower in late July and gave back some of the gains. The tech-heavy Nasdaq 100, which led markets higher in 1H 2024, returned -1.7% as Nvidia, Microsoft, Google, and Facebook-parent Meta traded down after their strong 2024 start. In contrast, the Russell 2000 Index of small-cap stocks posted its strongest monthly return since December 2023. In the bond market, Treasury yields fell. The U.S. Bond Aggregate Index, which tracks a wide array of investment-grade bonds, traded higher for a third consecutive month, the longest win streak since 2021. Despite the muted headline returns, the stock market experienced a seismic shift as expectations increased for a September interest rate cut.

Investors Rotate into Small Cap Stocks as Rate Cuts Come into View

Large-cap stocks dominated in the first half of 2024, with the S&P 500 outperforming the Russell 2000 by over +13%. The S&P 500’s strong first half return was influenced by two factors: (1) investor concerns about the impact of high interest rates on smaller companies and (2) large-cap stock indices’ exposure to the artificial intelligence (AI) industry. This combination of interest rate concerns and AI dominance led to crowded positioning as investors focused on a narrow group of large-cap stocks.

The investment narrative changed in July after the CPI inflation report showed continued progress. The better-than-expected inflation report raised expectations for a September interest rate cut, leading to a significant rotation within equity markets. Investors moved from large-cap stocks into small caps, with the Russell 2000 outperforming the S&P 500 by over +9%. This year’s high-flying mega-caps bore the brunt of the large-cap sell-off as investors questioned when billions of dollars in AI investments will pay off. As investors rotated, the year-to-date return gap between the Nasdaq 100 and Russell 2000 shrank from nearly +16% at the end of June to now only +3.3%. It’s uncommon for the stock market to experience such a large shift in such a short amount of time. There could be some residual volatility in the near term as markets weigh the prospects for corporate earnings and interest rate cuts, but the market isn’t expecting a repeat in August.