Welcome to Emergent Wealth Advisors’ monthly market summary! This past month, key takeaways included:

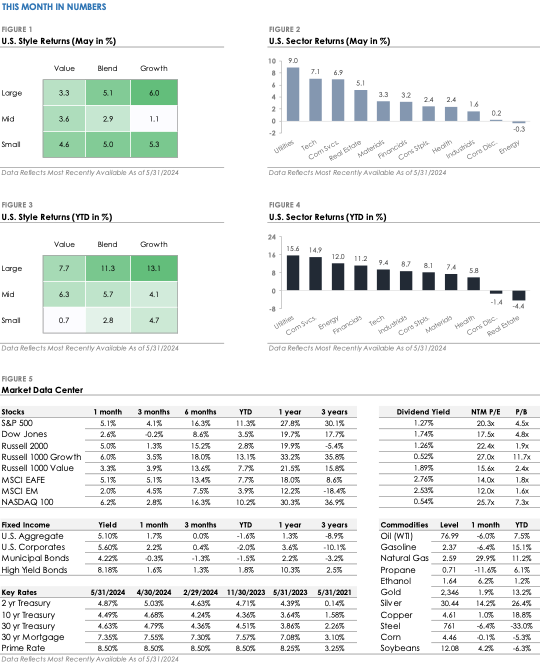

The S&P 500 Index gained +5.1%, slightly outperforming the Russell 2000 Index’s +5.0% return. Ten of the eleven S&P 500 sectors traded higher, led by Utilities.

Corporate investment-grade bonds produced a +2.2% total return as Treasury yields fell, outperforming the corporate high-yield bond index’s +1.6% total return.

International stock performance was varied. The MSCI EAFE developed market stock index returned +5.1%, while the MSCI Emerging Market Index returned +2.0%.

Stocks and Bonds Rebound in May Driven by Mega-Cap Technology

The S&P 500 set a new all-time high in May after trading lower in April. The technology-heavy Nasdaq 100 Index gained +6.2% and set a new all-time high, with mega-cap stocks like Nvidia, Apple, Microsoft, and Facebook-parent Meta leading the recovery. Notably, smaller companies also participated in the rally, with the Russell 2000 Index now showing positive YTD returns. In the credit market, Treasury yields reversed a portion of their April rise. The U.S. Bond Aggregate Index, which tracks a wide range of investment grade bonds, gained +1.7% as yields fell. What caused stocks and bonds to rebound after the April sell-off? The answer: Labor market and inflation data.

Shifting Economic Data Has Increased Market Volatility in 2Q 2024

The economy and Federal Reserve policy are in focus today. Investors are analyzing every new data point to extrapolate the trend. Labor market and inflation data are considered most relevant because the Fed aims for maximum employment and stable prices. Softer labor market data and lower inflation are viewed as pulling forward rate cuts, while stronger labor market data and higher inflation delay the expected timing of rate cuts.

In early April, the Labor Department reported that the U.S. added 315,000 jobs in March, causing unemployment to fall to 3.8%. A few weeks later, data showed Core CPI, which measures inflation excluding energy and food, held steady at 3.8% year-over-year. The combination of lower unemployment and unchanged inflation signaled a strong labor market and sticky inflation, leading investors to lower interest rate cut expectations.

In May, the latest labor market and inflation data signaled the opposite. The U.S. added 175,000 jobs, the slowest pace since October 2023, and unemployment rose to 3.9%. Inflation data revealed that Core CPI fell to 3.6% year-over-year, the lowest reading since April 2021. These data points marked a shift from the previous month, signaling a softer labor market and easing inflation. After lowering rate cut expectations in April, the market increased them in May. Treasury yields declined, and stocks traded higher.

As April and May showed, monthly economic data can be noisy. It can signal a strong trend one month and then the opposite trend the next month, causing investors to abruptly shift their views. This market volatility could continue over the summer until there is more certainty around Federal Reserve policy, inflation, and economic growth.