Monthly Market Summary

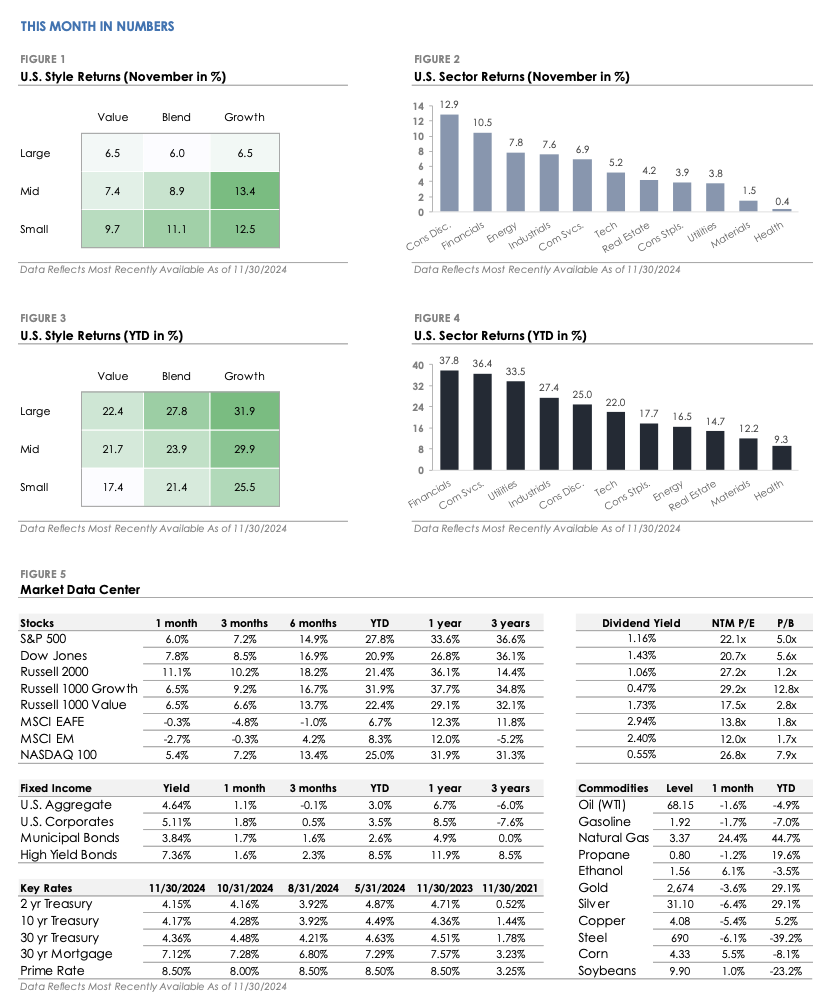

The S&P 500 Index returned +6.0% but underperformed the Russell 2000 Index’s +11.1% return. All eleven S&P 500 sectors traded higher, with Consumer Discretionary and Financials gaining more than +10%. In contrast, defensive sectors, such as Health Care, Utilities, and Consumer Staples, underperformed the S&P 500.

Corporate investment-grade bonds produced a +1.8% total return as Treasury yields declined, marginally outperforming corporate high-yield’s +1.6% total return.

International stocks traded lower for a second consecutive month. The MSCI EAFE developed market stock index returned -0.3%, while the MSCI Emerging Market Index returned -2.7%.

Markets Set New All-Time Highs in November’s Post-Election Rally

The U.S. presidential election results fueled November’s stock market rally, as investors focused on the incoming administration’s policy agenda and its implications. The S&P 500 gained +6.0%, its biggest monthly return since November 2023. The index traded above the key 6,000 level and set a new all-time high, bringing its year-to-date return to +27%. Smaller companies took center stage during the broad market rally, with the Russell 2000 surging +11.1% to set a record high. In the bond market, Treasury yields rose after the election due to concerns about increased fiscal spending, tax cuts, and large fiscal deficits under the next administration. However, later in the month, yields reversed lower, and bonds posted positive returns. With Republicans taking control of the White House, Senate, and House in January, the following section discusses key policy areas to watch, along with the potential market and economic impacts.

Key Policies to Watch in the Next Administration

Investors are monitoring two key areas: tax policy and trade. The administration is expected to focus on extending the tax cuts passed during President Trump’s first term. This could stimulate economic growth and boost corporate profits, although it could widen the fiscal deficit. On trade, the administration plans to use tariffs to advance U.S. interests in international affairs and renegotiate trade deals. However, in the near term, tariffs could disrupt supply chains, slow economic growth, and squeeze profit margins.

Other critical policies include immigration and deregulation. There are concerns that tariffs, stricter immigration policies, and expansionary fiscal policy could combine to keep inflation high. If so, the Federal Reserve might need to keep interest rates higher for longer. Elsewhere, there is an expectation that deregulation could create new growth opportunities in the financial and energy sectors, while relaxed antitrust enforcement could lead to more mergers and acquisitions. Economic growth and corporate earnings will remain important long-term drivers, but in the short term, markets may be sensitive to shifting policy headlines as the new administration takes office.